Source Credit : Portfolio Prints

Background

In December 2025, Netflix announced a definitive agreement to acquire Warner Bros.’ film and television studios, HBO, and the HBO Max streaming service in a blockbuster deal valued at about $82.7 billion (with an equity value of $72 billion) — a move widely described as effectively ending the “streaming wars.”

The transaction — one of the largest in entertainment history — combines Netflix’s global streaming scale with Warner Bros.’ century-long legacy of iconic franchises and premium TV content.

Why It’s Called the End of the Streaming Wars

The so-called streaming wars — a decade of intense competition among services like Netflix, Disney+, HBO Max, Paramount+, and Amazon Prime Video — pushed platforms to spend heavily on original and licensed content in an effort to attract and retain subscribers. Many analysts say that acquiring one of Netflix’s closest rivals could mark a decisive consolidation of that competition.

With Warner Bros.’ content — including DC, Game of Thrones, Friends, and Warner’s vast film and TV libraries — Netflix would control a huge share of premium streaming content globally, far surpassing most competitors and potentially putting a close on the era of fragmented platform competition.

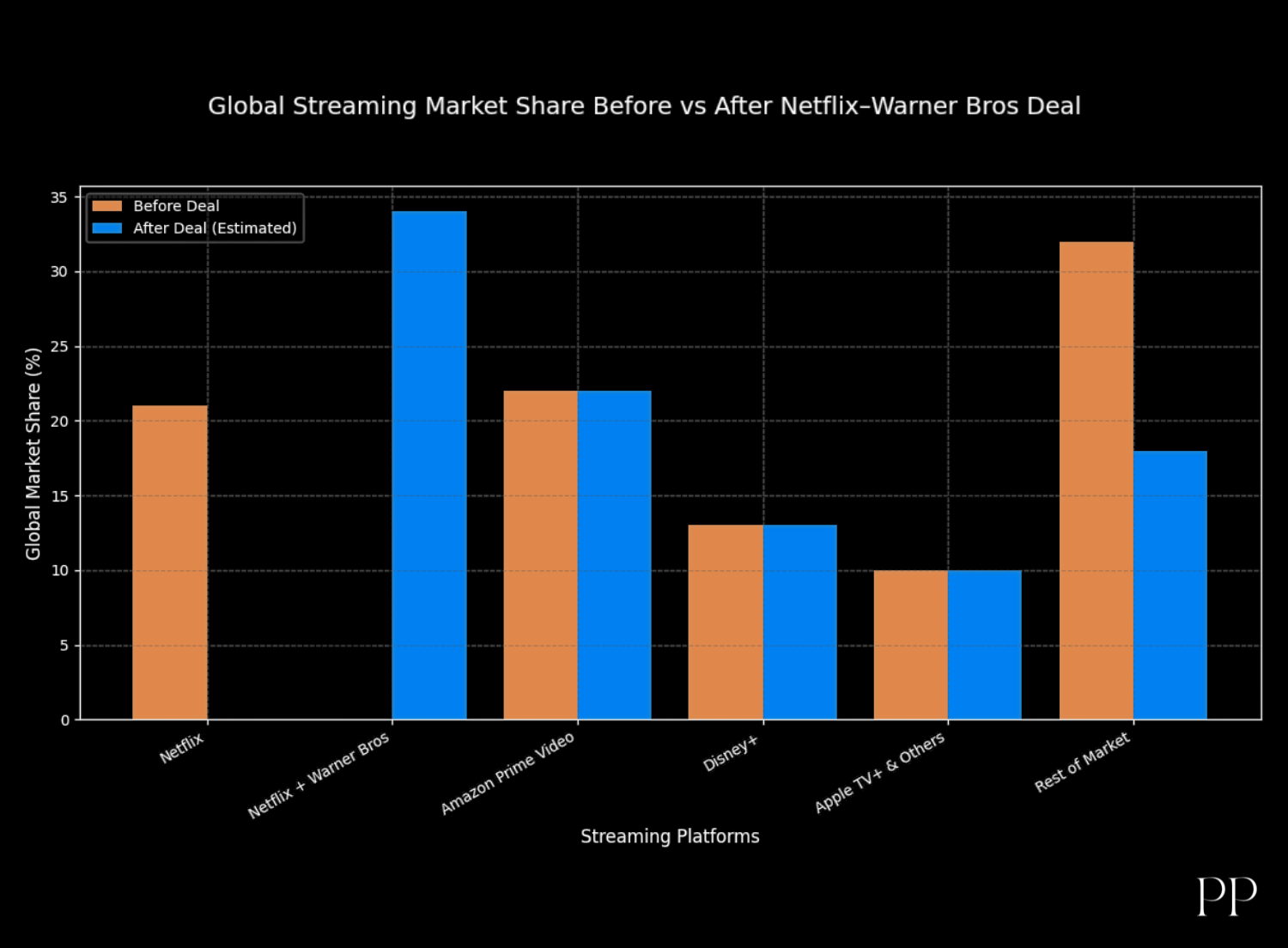

| Platform |

Before Deal |

After Deal |

| Netflix |

21 % |

~34 % (Netflix + HBO Max) |

| Amazon Prime Video |

22 % |

22 % |

| Disney+ |

12–14 % |

12–14 % |

| Apple TV+ & Others |

~9–11 % |

~9–11 % |

| Rest of Market |

~32 % |

~14–18 % |

Current Status (as of February 2026)

Shareholder Vote Expected

According to recent reporting, Warner Bros. Discovery shareholders are likely to vote on the transaction in March 2026. The vote is a critical step toward closing the deal.

Antitrust & Regulatory Scrutiny

Regulators are closely examining the proposed acquisition:

- The U.S. Department of Justice (DOJ) has launched an antitrust review, probing whether the deal would grant Netflix excessive market power and reduce competition in streaming.

- The DOJ’s actions include subpoenas and requests for information from competitors — a sign of serious competition concerns.

This review could delay or even block the merger under U.S. antitrust laws, similar to past major media mergers.

The Economics Behind Ending the Streaming Wars

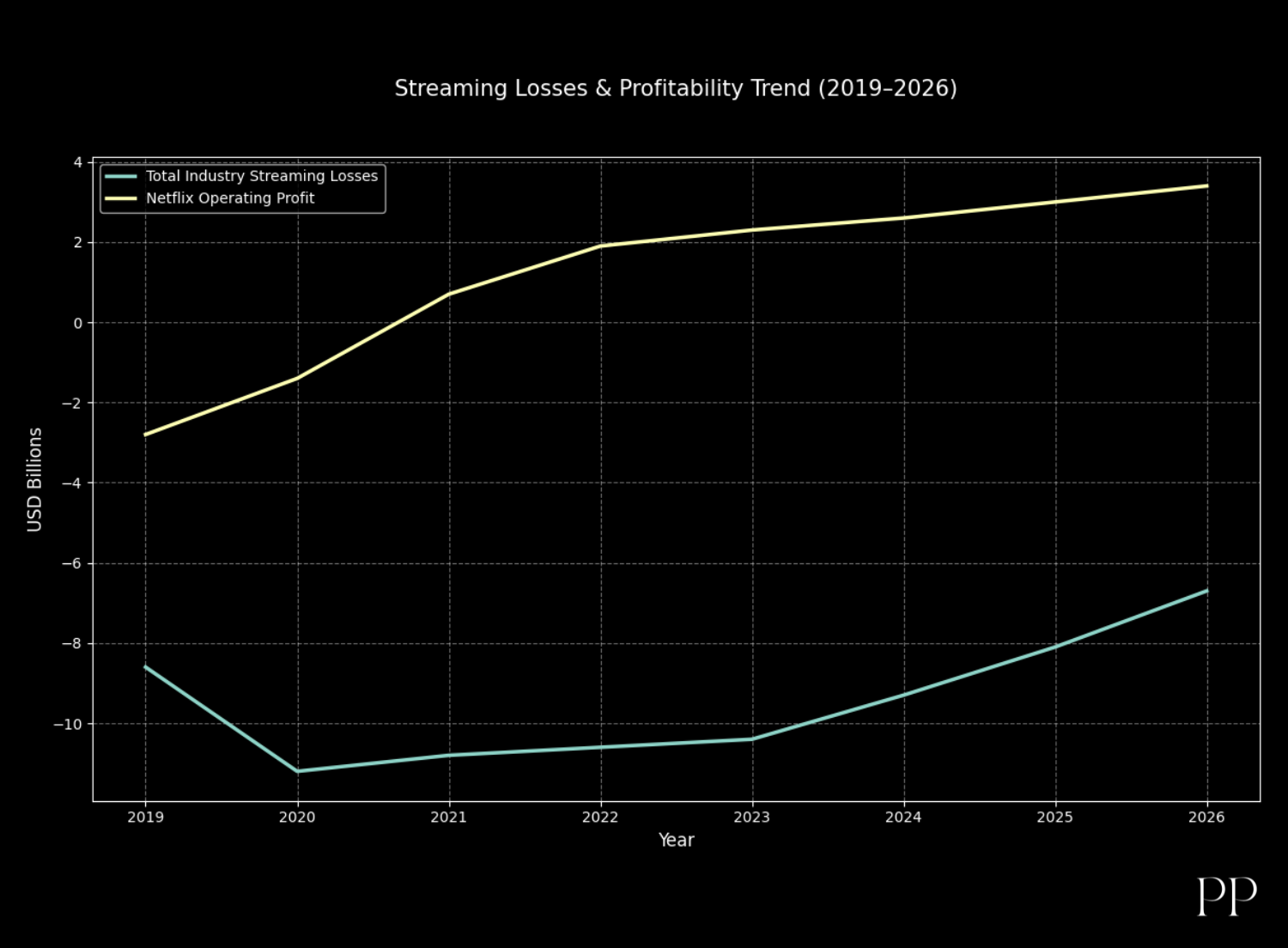

For nearly a decade, the global streaming industry ran on a single belief: scale first, profits later. Platforms poured billions into original content, global expansion, and aggressive pricing to win subscribers at any cost. That model worked—until it didn’t. By the mid-2020s, the economics of streaming began to crack, forcing companies to rethink strategy and accelerating consolidation across the industry.

Rising Content Costs vs. Slowing Subscriber Growth

At the heart of the problem was a widening gap between content spending and subscriber growth. Producing premium series and blockbuster films became dramatically more expensive, driven by talent costs, global production inflation, and competition for intellectual property. Annual content budgets for major platforms ballooned into the tens of billions of dollars.

At the same time, subscriber growth started to plateau—first in North America and Europe, and later even in key international markets. Most households willing to pay for multiple streaming services had already subscribed. Each new subscriber became harder and more expensive to acquire, while average revenue per user (ARPU) stagnated or rose only marginally due to price sensitivity.

The result was a classic scale problem: costs kept rising exponentially while growth followed a flatter curve.

Margin Pressure Across Streaming Platforms

As growth slowed, investors began focusing less on subscriber numbers and more on operating margins and free cash flow. This shift exposed how thin—and often negative—streaming margins really were.

- High fixed costs for content and technology

- Heavy marketing spend to retain users

- Low pricing power due to intense competition

Even industry leaders faced margin pressure, while legacy media companies struggled under the added weight of debt taken on during earlier mergers. Loss-making streaming divisions became increasingly difficult to justify to shareholders, especially in a higher interest-rate environment where capital was no longer cheap.

From “Growth at Any Cost” to Profitability

By the mid-2020s, Wall Street’s patience wore thin. The narrative decisively shifted from growth to profitability, efficiency, and consolidation. Platforms cut content budgets, cancelled underperforming shows, introduced advertising tiers, and raised prices—often at the cost of subscriber churn.

Consolidation emerged as the most logical solution. Combining platforms allowed companies to:

- Spread content costs across a larger subscriber base

- Eliminate duplicate spending on technology and marketing

- Monetize vast content libraries more efficiently

In this context, mega-deals like the Netflix–Warner Bros tie-up were not just strategic moves—they were economic necessities. The streaming wars didn’t end because competition disappeared; they ended because the old economics no longer worked.

Summary

The Netflix–Warner Bros. deal marks a turning point in the streaming industry, signaling the effective end of the so-called “streaming wars.” After years of aggressive content spending, mounting losses, and slowing subscriber growth, the economics of competing platforms became unsustainable. While Netflix shifted early toward profitability and cash flow discipline, rivals like Disney and Warner struggled with heavy losses and debt burdens. Faced with margin pressure and investor demands for returns, consolidation emerged as the logical solution. The merger reflects a broader industry shift—from growth at any cost to scale, efficiency, and sustainable profitability.