A Financial and Strategic Analysis of SpaceX IPO

Image Credit : Spacex

Source Credit : Portfolio Prints

Introduction

Since its establishment in 2002 by Elon Musk, SpaceX has fundamentally altered the economics of space transportation. Through reusable rocket technology, vertical integration, and aggressive innovation, the company reduced launch costs and established itself as the dominant launch provider worldwide. Over time, however, the company's strategic center of gravity shifted away from launch services toward satellite communications through Starlink.

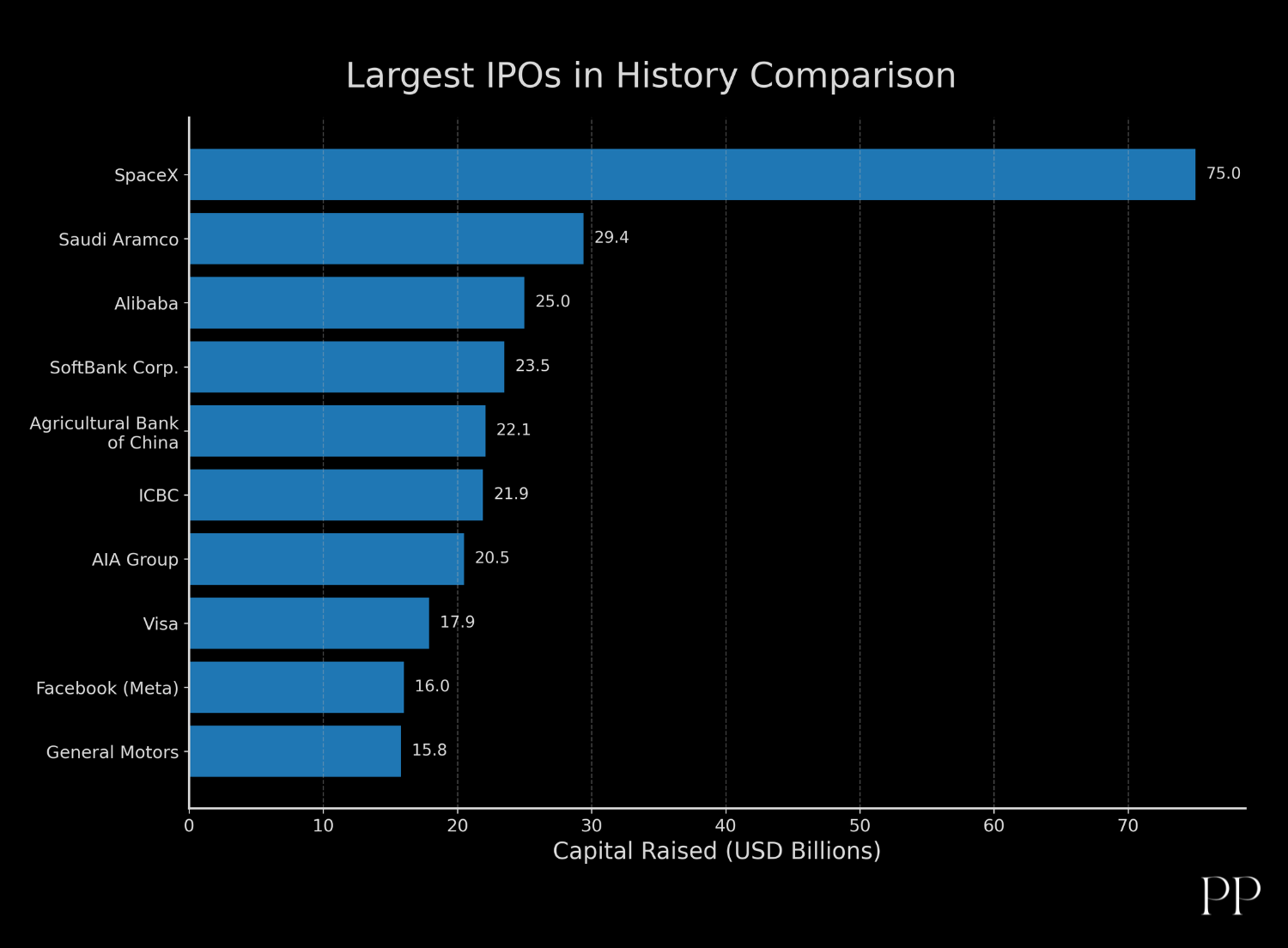

The SpaceX IPO is noteworthy not only because of its scale but also because it marks the first time investors have gained direct public-market access to a company that sits at the intersection of aerospace, telecommunications, artificial intelligence, defense technology, and digital infrastructure. Reuters reported that the company raised approximately $75 billion and debuted at a valuation near $2 trillion, making it the largest IPO in history.

Evolution of SpaceX's Business Model

SpaceX's development can be divided into three strategic phases.

The first phase focused on launch services through the Falcon rocket family. During this period, revenue was heavily dependent on commercial launch contracts and government agencies such as NASA and the U.S. Department of Defense.

The second phase involved the development of Starlink, a low-Earth-orbit satellite broadband network. Starlink transformed SpaceX from a project-based aerospace contractor into a recurring-revenue infrastructure provider.

The third phase, emerging between 2024 and 2026, integrated artificial intelligence and large-scale computing infrastructure into the broader SpaceX ecosystem, expanding the company's addressable market beyond aerospace and telecommunications.

| Period |

Core Business Focus |

Strategic Objective |

| 2002–2014 |

Launch Services |

Reduce launch costs |

| 2015–2022 |

Reusability & Government Contracts |

Achieve launch dominance |

| 2020–2025 |

Starlink Expansion |

Build recurring revenue |

| 2025–2030 |

AI, Connectivity & Space Infrastructure |

Create multi-industry platform |

IPO Structure and Market Reception

The IPO was preceded by years of speculation. Earlier reports suggested a valuation target between $1.5 trillion and $1.75 trillion. Subsequent investor demand pushed valuation expectations substantially higher before listing.

According to market reports, shares were priced around $135 and experienced a strong first-day appreciation, demonstrating significant investor enthusiasm despite concerns regarding profitability and governance.

| Metric |

Value |

| IPO Year |

2026 |

| IPO Valuation |

Approximately $2 Trillion |

| Capital Raised |

Approximately $75 Billion |

| IPO Price |

$135 per Share |

| Initial Trading Performance |

More than 20% gain after listing |

| Historical Ranking |

Largest IPO in History |

Sources indicate that investor demand was driven by expectations surrounding Starlink, future AI opportunities, and SpaceX's dominant competitive position in launch services.

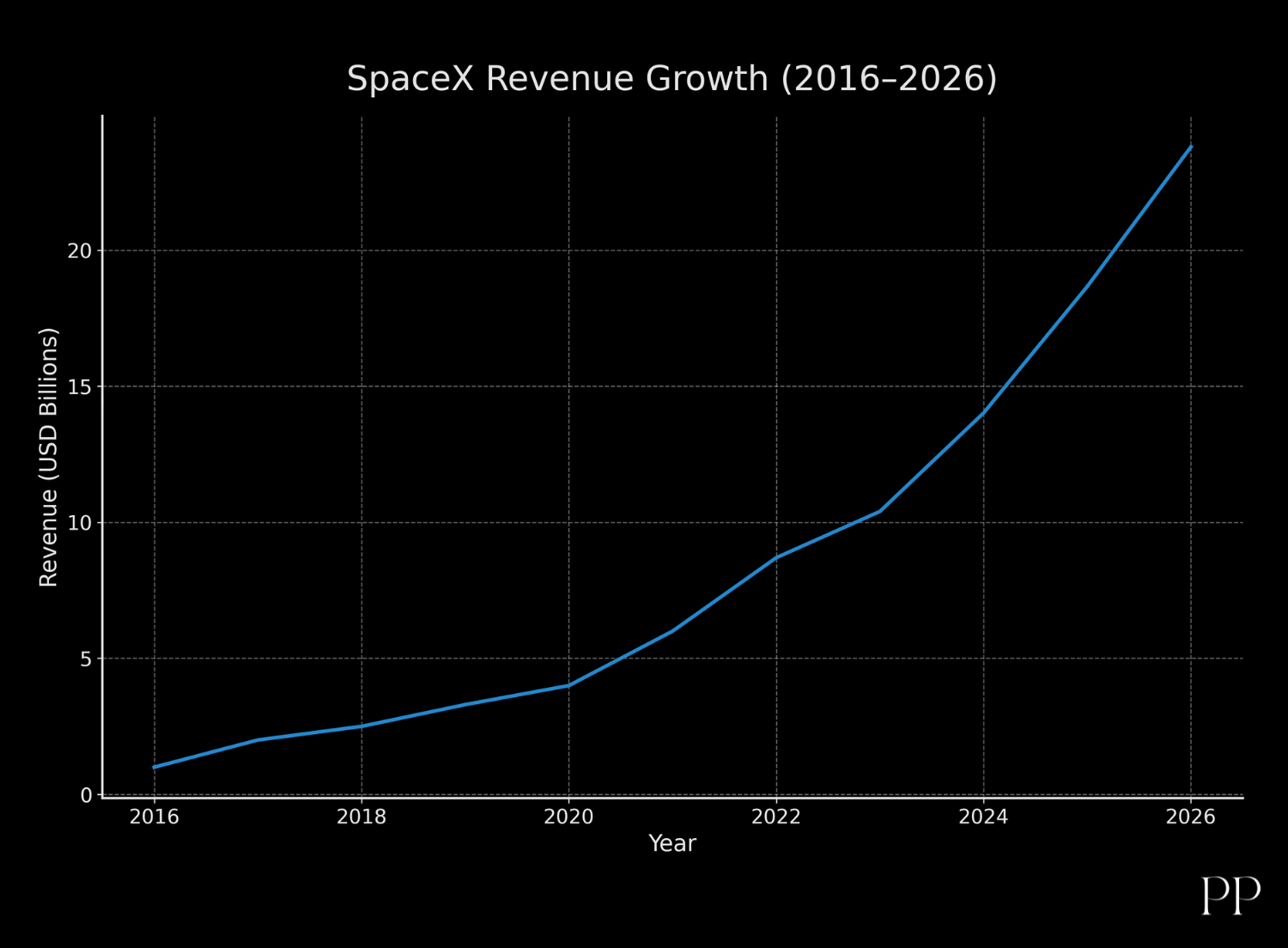

Financial Performance Analysis

A notable characteristic of SpaceX is the divergence between revenue growth and accounting profitability.

The company generated approximately $18.7 billion in revenue during 2025, representing significant year-over-year growth. However, substantial investments in AI infrastructure, satellite deployment, and next-generation launch systems have contributed to reported net losses.

| Financial Metric |

2023 |

2024 |

2025 |

| Revenue |

$10.4B |

$14.0B |

$18.7B |

| Growth Rate |

— |

34.6% |

33.6% |

| Adjusted EBITDA |

— |

$5.4B |

$6.6B |

| Net Income |

Negative |

Negative |

Negative |

| Capital Expenditure |

High |

Very High |

Extremely High |

Although profitability remains elusive under GAAP accounting standards, the company's EBITDA profile indicates strong operating leverage, particularly within the Starlink segment.

Revenue Segmentation

Research estimates suggest Starlink contributed approximately 60–65% of total company revenue in 2025 while generating the majority of operating profits. Launch operations remain strategically important but contribute a smaller share of overall earnings.

This distribution highlights a critical transformation: SpaceX is no longer primarily a rocket company. Instead, it increasingly resembles a global communications and infrastructure provider supported by aerospace capabilities.

This distribution highlights a critical transformation: SpaceX is no longer primarily a rocket company. Instead, it increasingly resembles a global communications and infrastructure provider supported by aerospace capabilities.

Valuation Analysis

One of the most debated aspects of the IPO is valuation.

At approximately $2 trillion, SpaceX trades at revenue multiples significantly above those of traditional aerospace companies. Reports indicate that valuation exceeded 100 times annual revenue, placing SpaceX closer to high-growth technology companies than aerospace peers.

Such valuation levels imply that investors are not valuing SpaceX based on current earnings but rather on expected future dominance in communications, orbital infrastructure, AI computing, and interplanetary transportation.

Risk Assessment

Despite its strengths, SpaceX faces substantial risks.

First, valuation risk remains significant. A $2 trillion valuation requires extraordinary future growth and execution. Even modest revenue disappointments could trigger substantial share-price volatility.

Second, governance concerns persist because voting control remains concentrated around Elon Musk. Investors may face limited influence over strategic decisions.

Third, technological risks remain elevated. Starship development, satellite replenishment cycles, launch failures, regulatory interventions, and geopolitical conflicts could materially affect future performance.

Fourth, increasing competition from satellite operators, telecommunications firms, and emerging launch providers may pressure margins over time.

Future Outlook and Growth Potential

The long-term investment thesis for SpaceX depends largely on Starlink, Starship, and AI infrastructure.

Industry forecasts suggest Starlink could surpass 15–20 million subscribers during the coming years while generating revenue substantially above current levels. Independent forecasts estimate company revenue could approach $22–30 billion within the near term if subscriber growth continues.

| Scenario |

Revenue Outlook (2030) |

Probability |

| Conservative |

$40–50B |

Moderate |

| Base Case |

$60–80B |

High |

| Optimistic |

$100B+ |

Moderate |

| Transformational |

$150B+ |

Low but Significant |

The transformational scenario assumes successful commercialization of Starship, expansion of Starlink enterprise services, AI infrastructure monetization, and new orbital economic activities.

Conclusion

The SpaceX IPO represents a watershed moment in both capital markets and the commercial space industry. Unlike traditional aerospace firms, SpaceX combines recurring subscription revenues, launch infrastructure, advanced manufacturing, satellite communications, and artificial intelligence under a single corporate structure. The company's financial profile demonstrates strong growth, substantial operating leverage within Starlink, and unmatched strategic positioning across multiple high-growth industries.

Nevertheless, the valuation embedded in the IPO reflects expectations extending far beyond current earnings power. Investors are effectively pricing SpaceX not as a launch company but as a future global infrastructure platform capable of dominating connectivity, orbital logistics, defense communications, and potentially interplanetary commerce. Whether those expectations are ultimately realized will determine whether the IPO becomes one of the greatest long-term investments in market history or an example of excessive optimism toward disruptive technology narratives.

From a research perspective, SpaceX remains one of the most strategically important and financially consequential companies of the twenty-first century, with implications extending well beyond aerospace into telecommunications, artificial intelligence, global infrastructure, and the future architecture of the digital economy.