Source Credit : Portfolio Prints

Background

India firmed up one of the most consequential policy pushes in its industrial history: a plan to begin domestic production of rare-earth permanent magnets by the end of 2026 while building dedicated rare earth corridors — a structural attempt to wrestle away China’s decades-long dominance over rare earths and critical mineral supply chains

This initiative is not just another industrial policy. It represents a geoeconomic pivot — linking national security, global competitiveness, and technological autonomy.

What Are Rare Earths and Why They Matter

Rare earth elements (REEs) comprise 17 metallic elements critical to today’s high-tech world — from smartphones and medical devices to electric vehicles (EVs), wind turbines, aerospace systems, and advanced defence platforms. They include neodymium, dysprosium, terbium, and others used in magnets, sensors, catalysts, and lasers.

Despite their name, these minerals are not geologically rare; the challenge lies in their extraction, refining, processing, and manufacturing — all of which require resource-intensive technology and environmental controls.

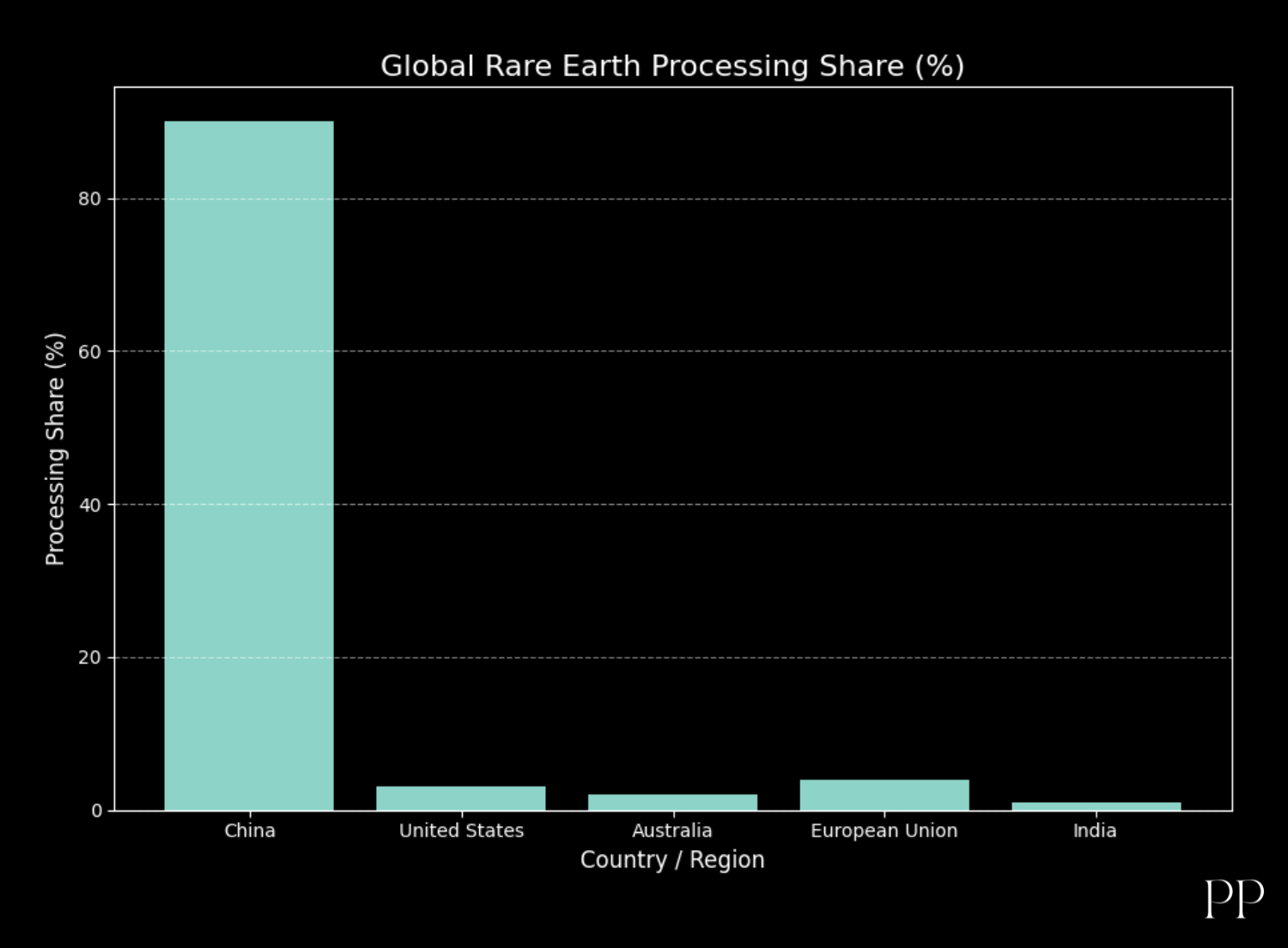

China’s Historic Dominance

China’s role in the global rare earth supply chain is unparalleled:

- China accounts for roughly 60–70% of global REE mining output and about 90% of processing capacity.

- This dominance is the outcome of four decades of state-led investment, deep industrial integration, and patent accumulation in extraction and separation technologies.

China’s control enables it to set global prices, restrict exports, and exert strategic leverage — factors that have repeatedly surfaced in trade tensions, notably with the United States and other advanced economies.

Such chokehold has often left other countries vulnerable. For example, China’s export restrictions on magnets and certain rare earth elements disrupted industries worldwide, including automobile manufacturers and clean energy sectors.

Such chokehold has often left other countries vulnerable. For example, China’s export restrictions on magnets and certain rare earth elements disrupted industries worldwide, including automobile manufacturers and clean energy sectors.

India’s Strategic Response: Rare Earth Corridors & Magnet Production

Dedicated Rare Earth Corridors

The Union Budget 2026-27 introduced rare earth corridors — integrated industrial clusters designed to co-locate mining, processing, research, and manufacturing in states such as Odisha, Kerala, Andhra Pradesh, and Tamil Nadu.

These corridors aim to overcome a structural flaw: India has rich deposits (about 6.9 million tonnes) and is the third-largest holder of rare earth reserves globally, yet contributes only a fraction of global production.

The corridors are intended to create end-to-end domestic value chains, attract private and foreign capital, and develop technical expertise.

Rare Earth Permanent Magnets Manufacturing

Perhaps the boldest part of India’s plan is to start producing rare earth permanent magnets domestically by late 2026, backed by a ₹73 billion (~$802 million) programme.

Permanent magnets — especially neodymium-iron-boron (NdFeB) magnets — are the linchpin of modern electrification:

- EV motors

- Hard disk drives

- Aerospace systems

- Wind turbines

- Defence actuators

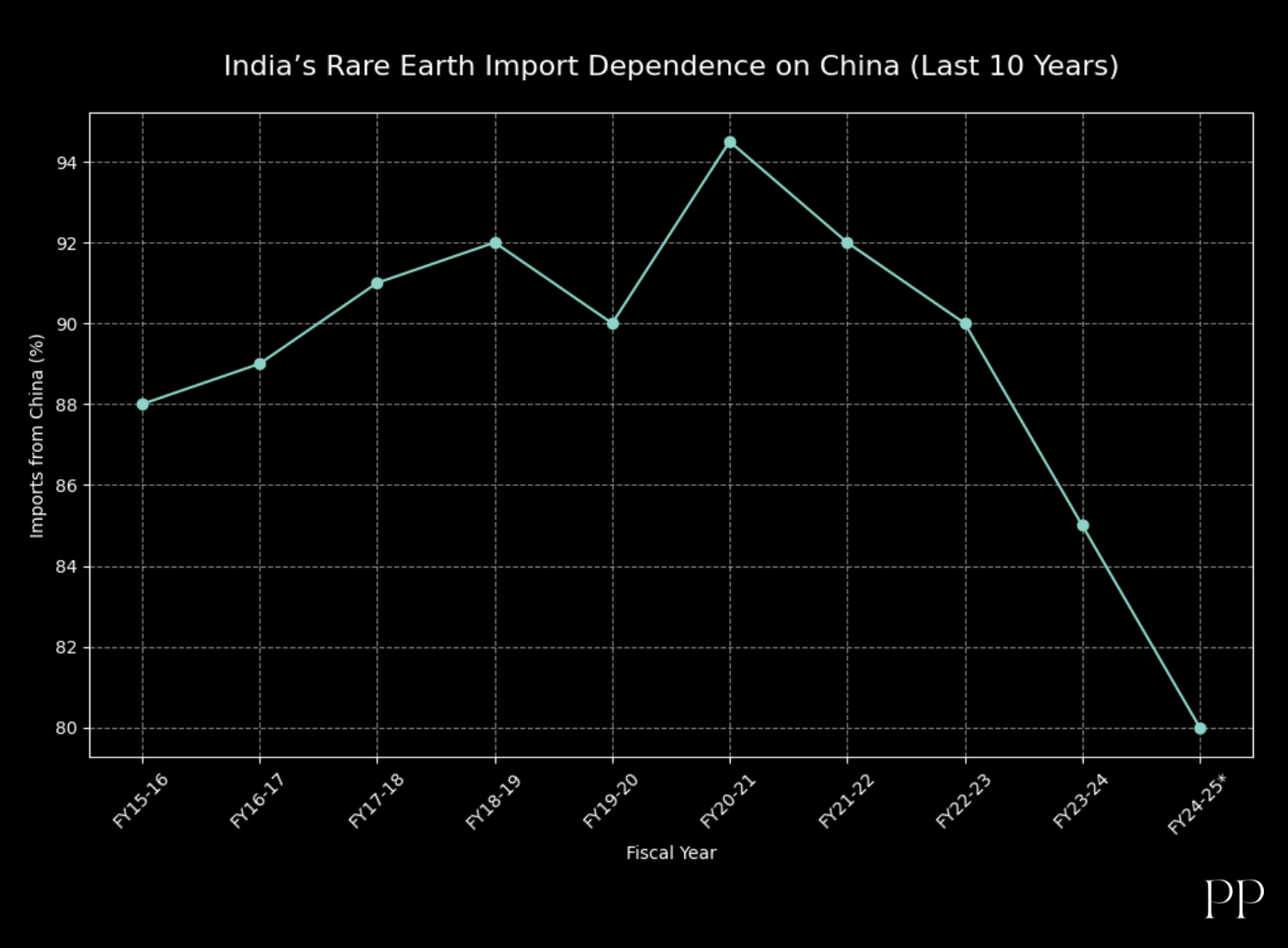

Until now, India has imported 60–90% of its magnet needs from China by volume and value.

| Fiscal Year |

% Share of India’s Rare Earth Imports from China |

| FY 2019–20 |

~90% |

| FY 2020–21 |

≈94.5% (peak dependence) |

| FY 2021–22 |

~92% |

| FY 2022–23 |

~90% |

| FY 2023–24 |

≈59% (share declines as alternative suppliers contribute more) |

| CY 2023 (calendar) |

~88% |

| CY 2024 (latest trade data) |

~80% |

Economic and Strategic Stakes

Industrial Growth and Job Creation

Domestic rare earth industries can generate high-value jobs across mining, metallurgy, processing, and manufacturing. Coupled with industrial research and scale economies, this sector could become a significant contributor to India’s growth story.

Reducing External Vulnerability

Excessive dependence on a single country for critical inputs is a strategic vulnerability. When China imposed export curbs and licensing requirements on rare earth exports, global supply chains buckled, threatening production lines in several major economies.

India’s push is part of a larger strategic recalibration — diversifying supply, securing resources, and building domestic capacity.

Challenges and Bottlenecks

Technological Gaps

China’s leadership was built on decades of technology development, infrastructure, and patent depth. India, by contrast, must rapidly build processing expertise — a non-trivial undertaking that requires research, capital, and partnerships.

Investment and Expertise

Rare earth processing is capital-intensive, and mining operations demand environmental safeguards due to the toxic nature of some by-products. Public-private partnerships or foreign collaboration may be necessary to bridge expertise and investment gaps.

Environmental and Community Concerns

Mining and processing carry environmental risks. Building responsible supply chains with environmental standards and local community consent will be critical for sustainable long-term success.

Geopolitical Dimensions

India’s rare earth strategy is not only an economic plan — it’s a geopolitical maneuver:

- It aligns with U.S. and other democracies’ efforts to diversify supply away from China. India joined global efforts such as the Critical Minerals Ministerial alongside the U.S. and others.

- It potentially opens collaboration with Western allies, technology partners, and alternative raw material suppliers in Africa, Latin America, and Southeast Asia.

- By asserting production capabilities, India strengthens its influence in critical mineral diplomacy — a strategic tool for 21st-century geopolitics.

Conclusion

India’s rare earth corridors initiative marks a strategic watershed moment. It combines industrial policy, national security, and geopolitical ambition in one comprehensive strategy to break free from China’s decades-long monopoly in critical minerals.

While challenges remain — from technology gaps to investment hurdles — the initiative represents India’s determination to assert autonomy in the most strategically sensitive industrial domain of the 21st century. If successful, it will not only fortify India’s supply chains but also realign global rare earth dynamics more equitably — a shift with profound implications for technology, defence, and international power balances.