Source Credit : Portfolio Prints

Overview

Europe’s energy markets have experienced dramatic upheavals since the 2022 trigger of the energy crisis following Russia’s invasion of Ukraine. At that time, soaring gas and electricity prices dealt a severe blow to consumers and businesses alike, pushing energy costs to levels that risked hollowing out the continent’s industrial base. In response, policymakers pursued emergency interventions, diversification of supply, and accelerated renewables deployment.

Now, in early 2026, a cautious—but meaningful—reduction in energy prices is underway, prompting both optimism and urgency in industry and government circles. While prices are still above historic norms, they have eased significantly from peak crisis levels, creating a potentially pivotal moment for industrial competitiveness and strategic economic renewal.

The Price Trend

Energy Price Trajectory

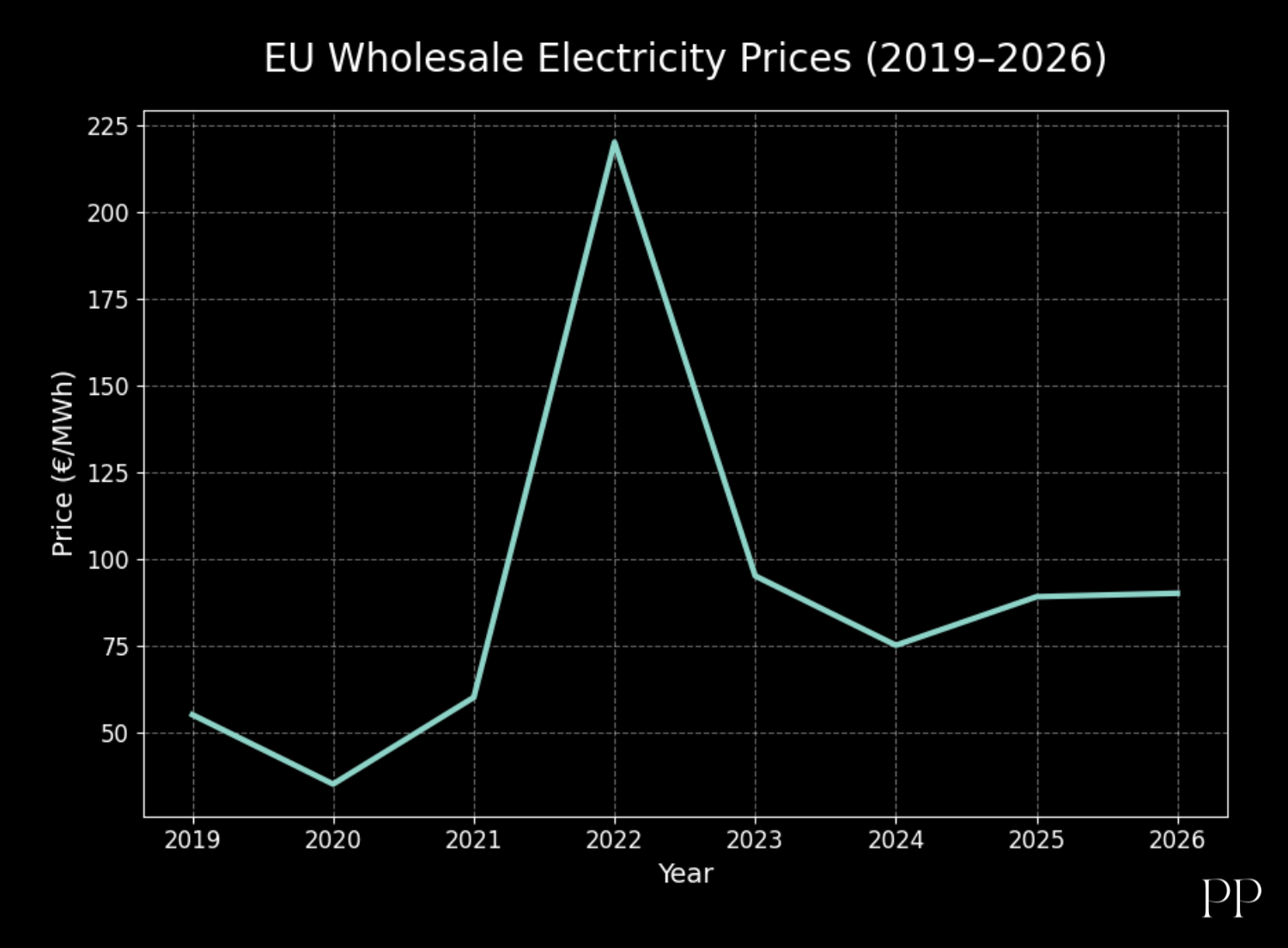

- Wholesale prices—still elevated but down: Average wholesale electricity prices in parts of Europe have declined from their crisis-era highs (where they occasionally surpassed €400/MWh) to an average closer to €80-€90/MWh, and gas prices now trade near €30-€35/MWh in many markets. This represents a sharp correction from the worst of the 2022-23 crisis.

- Industrial energy cost pressures persist: Eurostat and independent data show that, despite recent reductions, industrial energy producer prices are still cumulatively around 66% higher than in early 2021—before the crisis began. That means the competitive gap with global rivals hasn’t disappeared, just narrowed.

Why Prices Have Eased

Several factors underpin the price correction:

- Warm seasons and milder winters lowering heating demand.

- Renewables generating a growing share of electricity, easing dependence on expensive gas during peak periods.

- Expansion of LNG supply sources and deeper gas storage levels.

- Policy measures and market reforms aimed at weakening the direct link between electricity and fossil fuel prices.

However, volatility remains, with weather, wind output variability, and carbon costs continuing to influence price dynamics.

Deindustrialization Pressures

The industrial sectors of Europe—especially energy-intensive industries like steel, chemicals, cement, and metals—have long warned that persistent high energy costs threaten competitiveness, investment, and jobs.

Industrial Warnings and Job Losses

In mid-February 2026, a broad coalition of energy-intensive industries issued a stark statement urging the EU to take immediate action to avert what they describe as “irreversible deindustrialisation.” They pointed to:

- Energy costs (both electricity and carbon) remaining roughly twice as high as in key global markets.

- Production declines of up to 40% in some sectors compared to 2018 levels.

- A cumulative loss of about 1.5 million jobs in energy-intensive sectors since 2008.

Factory Closures and Capacity Loss

Extended high prices have already contributed to the closure of many industrial facilities, the loss of tens of thousands of jobs, and the disappearance of millions of tonnes of chemical production capacity across Europe.

Policy Responses

Europe’s leaders and institutions are acutely aware that tackling high energy costs is now central to preserving the continent’s industrial future. Actions fall into several categories:

Short-Term Price Relief Measures

Government packages: For example, Italy adopted a €3 billion package in February 2026 aimed at cutting wholesale energy prices, including targeted subsidy schemes and adjustments to the corporate tax regime to fund consumer and industrial relief.

EU-wide coordination: The European Commission’s Energy Union Task Force is coordinating actions to reduce energy prices, accelerate permitting for projects, expand interconnections, and recalibrate taxes and levies.

Structural and Long-Term Policy Reforms

Electricity market reform: EU leaders are considering reforms to decouple electricity prices from expensive gas price triggers, which could help stabilize costs for industry and consumers.

Clean Industrial Deal and Affordable Energy Plan: These frameworks built around 2025 aim to deliver both short-term price relief and long-term structural competitiveness by promoting home-grown clean energy and reducing system costs.

State aid facilitation: Updated EU state-aid rules now permit direct industrial electricity subsidies in member states like Germany, reflecting a broader shift toward compensating industry without breaching EU competition rules.

Integrated Climate and Competitiveness Strategy

Despite tensions between environmental policies and competitiveness concerns, the EU is seeking policy balance. Efforts to adapt the EU Emissions Trading System (ETS) and manage carbon cost burdens are central to this, although debates continue over timing and market design.

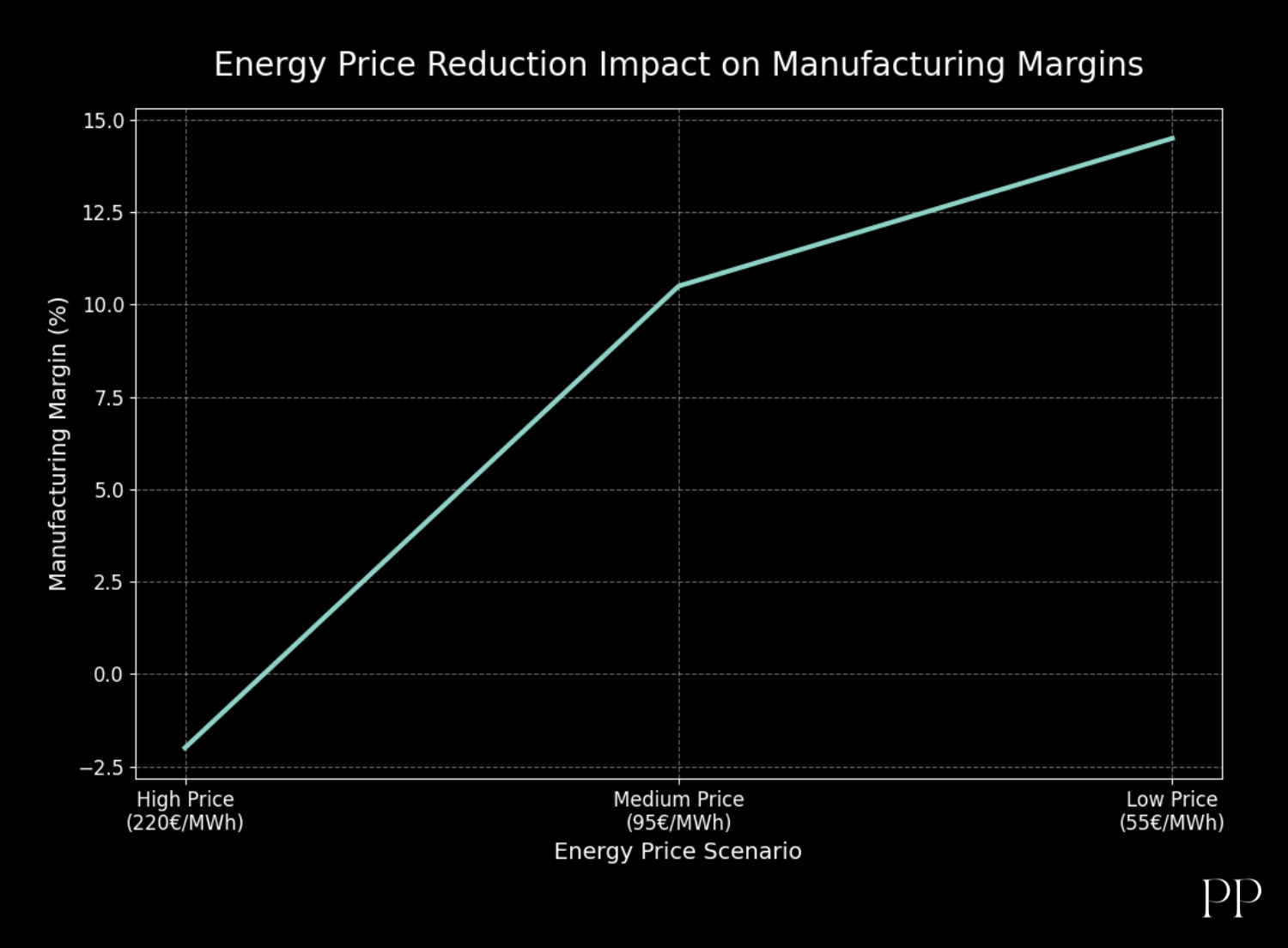

Margin = Revenue − (Non−energycosts + Energycost)

| Scenario |

Electricity Price (€/MWh) |

Manufacturing Margin (€) |

Margin % |

| High Price |

220 |

-20 |

-2.0% |

| Elevated |

95 |

105 |

10.5% |

| Moderate |

75 |

125 |

12.5% |

| Low |

55 |

145 |

14.5% |

| Target Level |

40 |

160 |

16.0% |

Opportunities in a Lower-Price Era

Renewables and Decarbonized Production as Competitive Assets

Europe is rapidly expanding renewable energy capacity, which not only reduces reliance on imported fossil fuels but also promises more stable and lower-cost electricity in the long run. For instance, solar and wind generation hit new records in 2025, pushing down price pressures in specific periods.

Regional Specialization and Energy Hubs

Areas with strong renewable potential—such as the Iberian Peninsula—have potential to become green industrial hubs, exporting reliable low-cost clean energy and attracting investment in energy-intensive manufacturing linked to decarbonization.

Infrastructure and Interconnections

Investment in grid flexibility, storage solutions, and cross-border interconnections can smooth out volatility and enable cheaper energy to reach high-demand industrial zones.

Conclusion

Europe’s recent reductions in energy prices, while incomplete, represent a critical window of opportunity. If policymakers can translate short-term relief into well-designed long-term reforms, the continent could:

- Reverse some of the competitive loss suffered over recent years.

- Attract new investment into energy-intensive and strategic industrial sectors.

- Strengthen its economic and strategic autonomy by anchoring manufacturing to cleaner, cheaper domestic energy sources.

Conversely, failure to act decisively risks cementing competitive disadvantage and deepening deindustrialization trends that have been visible across major economies such as Germany and other EU states.

Energy price reductions are more than a cyclical relief—they represent a strategic inflection point. Europe now faces a choice: seize this moment with comprehensive policy action to rebuild industrial competitiveness, or watch opportunities slip away as global rivals outperform on cost and capacity.