US Services PMI increases 0.9% point to 54.5 in May

Image Credit : Bloomberg

Source Credit : Portfolio Prints

U.S. services sector activity accelerated in May as businesses moved aggressively to secure supplies and rebuild inventories amid growing concerns over shortages and rising costs linked to the ongoing conflict in the Middle East.

Data released Wednesday by the Institute for Supply Management (ISM) showed that service-sector growth strengthened last month, while a key measure of input costs climbed to its highest level in nearly four years. Businesses reported sharp increases in petroleum-related expenses, a concern that was notably absent from April's survey responses.

The economic impact of the three-month U.S.-backed conflict with Iran is increasingly being felt across global supply chains. Disruptions in commodity markets have driven up prices for energy products, aluminum, fertilizers, and other critical inputs, creating fresh inflationary pressures throughout the economy.

Those concerns were echoed in the Federal Reserve's latest Beige Book, which reported that prices rose at a "moderate to strong pace" during May. According to the report, higher energy costs tied to the Middle East conflict were the primary source of inflationary pressure, with ripple effects extending into transportation, packaging, groceries, and agricultural products.

As inflation risks mount, financial markets increasingly expect the Federal Reserve to keep interest rates elevated for an extended period, with no significant policy easing anticipated before 2027.

"The largest segment of the economy continues to expand at a healthy pace, even as inflation pressures intensify," said Priscilla Thiagamoorthy, Senior Economist at BMO Capital Markets. "That combination is likely to keep Federal Reserve officials firmly in wait-and-see mode."

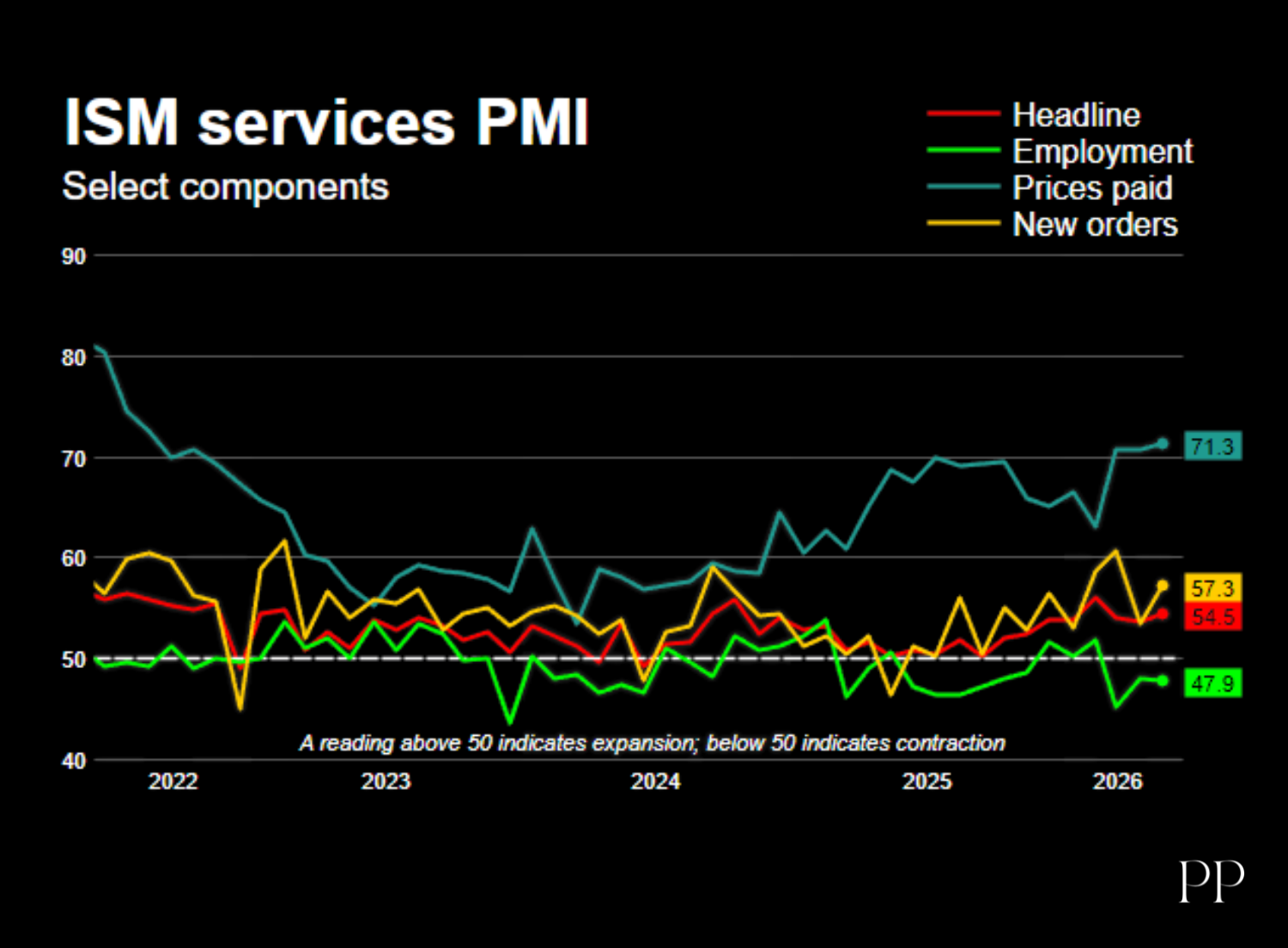

The ISM's Non-Manufacturing Purchasing Managers Index (PMI) rose to 54.5 in May from 53.6 in April, exceeding economists' expectations of 53.8. Any reading above 50 signals expansion.

The stronger performance highlights continued resilience in the services sector, which accounts for more than two-thirds of U.S. economic activity. The gain also follows a recent rebound in manufacturing activity, suggesting broader economic momentum despite rising geopolitical risks.

Seventeen industries reported growth during the month, including wholesale trade, construction, public administration, accommodation and food services, utilities, and retail trade. Real estate, rental, and leasing was the only major industry reporting contraction.

However, comments from businesses revealed growing concern about inflation and emerging supply bottlenecks.

Educational service providers reported increasing shortages and rising costs for construction materials, computers, laptops, and tablets. Meanwhile, companies in the accommodation and food services sector said suppliers were attempting to pass through higher fuel surcharges and rising costs for petroleum-based products.

"We expect significant cost increases to impact operations by late second quarter and certainly into the third quarter," one respondent noted.

Wholesale trade firms reported delays and revisions to major energy-related capital expenditure projects, citing macroeconomic uncertainty. At the same time, surging demand from data-center power generation projects has tightened inventory availability across key industrial supply markets.

One of the survey's most striking developments was a sharp rise in inventories.

The services-sector inventory index surged to 62.5, its highest level since May 2010, compared with 53.1 in April. The increase suggests many companies are stockpiling goods in anticipation of future supply disruptions and higher costs.

The surge follows four consecutive quarters of declining business inventories—the longest such stretch since the Great Recession.

According to Steve Miller, Chair of the ISM Services Business Survey Committee, the inventory buildup does not signal weakening demand. Instead, he said, businesses appear confident that economic activity will remain strong despite rising costs.

That confidence was reflected in new orders, which jumped to 57.3 from 53.5 in April. Backlog growth and export activity, however, moderated somewhat during the month.

Perhaps the most concerning aspect of the report was the continued rise in input costs.

The ISM's Prices Paid Index climbed to 71.3 in May, the highest reading since August 2022 and well above levels typically associated with elevated inflation.

The increase suggests that the recent energy shock is spreading beyond commodity markets and into the broader services economy. Businesses are increasingly facing higher operating costs, many of which are expected to be passed on to consumers.

Supplier deliveries remained unusually slow, though the index eased slightly to 55.2 from 56.8 in April. Readings above 50 indicate slower deliveries.

While stronger demand can often contribute to slower delivery times, businesses reported that ongoing supply-chain disruptions were the primary factor. Shortages of computers, electronic components, and memory chips remained widespread.

Despite solid business activity, hiring across the services sector remained subdued.

The ISM reported that many companies continue to implement hiring freezes or are choosing not to replace departing employees. The trend aligns with the Federal Reserve's Beige Book, which described labor conditions as a "low-hire, low-fire" environment characterized by selective recruitment focused primarily on critical positions.

Separate data from the ADP National Employment Report showed private-sector employment increased by 122,000 jobs in May, following a gain of 105,000 in April.

Economists remain cautious about interpreting the ADP figures, however, as the report has historically been a weak predictor of the government's official employment data.

Additional labor-market indicators paint a mixed picture. The latest Job Openings and Labor Turnover Survey (JOLTS) showed hiring slowed and layoffs declined in April, suggesting employment growth has been supported more by reduced job losses than by stronger hiring demand.

Economists surveyed by Reuters expect nonfarm payrolls to have increased by 85,000 jobs in May, while the unemployment rate is projected to remain unchanged at 4.3%.

Samuel Tombs, Chief U.S. Economist at Pantheon Macroeconomics, noted that several leading indicators of employment have weakened in recent months.

"Measures with stronger forecasting records—including small-business hiring intentions, regional Federal Reserve surveys, and consumer perceptions of job availability—have all softened," Tombs said. "Evidence that the labor market is regaining meaningful momentum remains limited."

The latest data suggest the U.S. economy remains resilient despite mounting geopolitical uncertainty. Strong demand, rising new orders, and aggressive inventory rebuilding point to continued expansion across the services sector.

Yet the same report also highlights growing risks. Inflationary pressures are intensifying, supply chains are becoming more strained, and businesses are increasingly preparing for prolonged disruptions stemming from the Middle East conflict.

For Federal Reserve policymakers, the combination of solid economic growth and accelerating price pressures may leave little room for near-term interest-rate cuts, ensuring that monetary policy remains restrictive even as businesses navigate an increasingly uncertain global environment.

The stronger performance highlights continued resilience in the services sector, which accounts for more than two-thirds of U.S. economic activity. The gain also follows a recent rebound in manufacturing activity, suggesting broader economic momentum despite rising geopolitical risks.

Seventeen industries reported growth during the month, including wholesale trade, construction, public administration, accommodation and food services, utilities, and retail trade. Real estate, rental, and leasing was the only major industry reporting contraction.

However, comments from businesses revealed growing concern about inflation and emerging supply bottlenecks.

Educational service providers reported increasing shortages and rising costs for construction materials, computers, laptops, and tablets. Meanwhile, companies in the accommodation and food services sector said suppliers were attempting to pass through higher fuel surcharges and rising costs for petroleum-based products.

"We expect significant cost increases to impact operations by late second quarter and certainly into the third quarter," one respondent noted.

Wholesale trade firms reported delays and revisions to major energy-related capital expenditure projects, citing macroeconomic uncertainty. At the same time, surging demand from data-center power generation projects has tightened inventory availability across key industrial supply markets.

One of the survey's most striking developments was a sharp rise in inventories.

The services-sector inventory index surged to 62.5, its highest level since May 2010, compared with 53.1 in April. The increase suggests many companies are stockpiling goods in anticipation of future supply disruptions and higher costs.

The surge follows four consecutive quarters of declining business inventories—the longest such stretch since the Great Recession.

According to Steve Miller, Chair of the ISM Services Business Survey Committee, the inventory buildup does not signal weakening demand. Instead, he said, businesses appear confident that economic activity will remain strong despite rising costs.

That confidence was reflected in new orders, which jumped to 57.3 from 53.5 in April. Backlog growth and export activity, however, moderated somewhat during the month.

Perhaps the most concerning aspect of the report was the continued rise in input costs.

The ISM's Prices Paid Index climbed to 71.3 in May, the highest reading since August 2022 and well above levels typically associated with elevated inflation.

The increase suggests that the recent energy shock is spreading beyond commodity markets and into the broader services economy. Businesses are increasingly facing higher operating costs, many of which are expected to be passed on to consumers.

Supplier deliveries remained unusually slow, though the index eased slightly to 55.2 from 56.8 in April. Readings above 50 indicate slower deliveries.

While stronger demand can often contribute to slower delivery times, businesses reported that ongoing supply-chain disruptions were the primary factor. Shortages of computers, electronic components, and memory chips remained widespread.

Despite solid business activity, hiring across the services sector remained subdued.

The ISM reported that many companies continue to implement hiring freezes or are choosing not to replace departing employees. The trend aligns with the Federal Reserve's Beige Book, which described labor conditions as a "low-hire, low-fire" environment characterized by selective recruitment focused primarily on critical positions.

Separate data from the ADP National Employment Report showed private-sector employment increased by 122,000 jobs in May, following a gain of 105,000 in April.

Economists remain cautious about interpreting the ADP figures, however, as the report has historically been a weak predictor of the government's official employment data.

Additional labor-market indicators paint a mixed picture. The latest Job Openings and Labor Turnover Survey (JOLTS) showed hiring slowed and layoffs declined in April, suggesting employment growth has been supported more by reduced job losses than by stronger hiring demand.

Economists surveyed by Reuters expect nonfarm payrolls to have increased by 85,000 jobs in May, while the unemployment rate is projected to remain unchanged at 4.3%.

Samuel Tombs, Chief U.S. Economist at Pantheon Macroeconomics, noted that several leading indicators of employment have weakened in recent months.

"Measures with stronger forecasting records—including small-business hiring intentions, regional Federal Reserve surveys, and consumer perceptions of job availability—have all softened," Tombs said. "Evidence that the labor market is regaining meaningful momentum remains limited."

The latest data suggest the U.S. economy remains resilient despite mounting geopolitical uncertainty. Strong demand, rising new orders, and aggressive inventory rebuilding point to continued expansion across the services sector.

Yet the same report also highlights growing risks. Inflationary pressures are intensifying, supply chains are becoming more strained, and businesses are increasingly preparing for prolonged disruptions stemming from the Middle East conflict.

For Federal Reserve policymakers, the combination of solid economic growth and accelerating price pressures may leave little room for near-term interest-rate cuts, ensuring that monetary policy remains restrictive even as businesses navigate an increasingly uncertain global environment.